Time to recalibrate policy measures

By Alan Cheong

/ Savills |

When markets run amok, government policies are expected to provide stability. This was indeed the case when the policy measures first kicked in, starting from September 2009 and culminating in the implementation of the total debt service ratio (TDSR) framework on June 29, 2013. The market then started to respond to these measures and began the long process of detoxification.

The slew of measures has altered the real estate investment landscape and effectively constrained overspending. Consequently, the private residential market is now behaving in ways that are different from the heydays of the past.

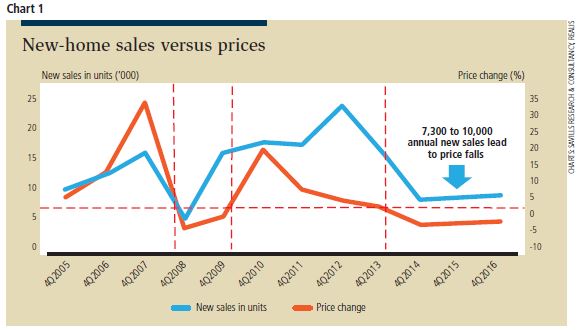

Here, we look at some of those changes. The sequential imposition of the cooling measures has inadvertently created a live experiment on its impact on new-home sales in conjunction with housing prices. Over the past 14 quarters, with the measures in place, annual new-home sales volume has hovered between 7,300 and 7,900 units, with price changes in negative territory.

Achieving an increase in transaction volume would merely require some adjustments to the current slate of cooling measures

Spike in sales volume unlikely to trigger a rapid asset price inflation

After TDSR came into force, new-home sales totalled 4,998 units — just half the 9,950 units sold in 1H2013. Prices also fell 0.5% from end- 1H2013 to end-2H2013. On an annualised basis, new-home sales volume post-TDSR should then be 9,996 units (4,998 units x 2) and price fall 1% (0.5% x 2). Therefore, even if new home sales were to increase to about 10,000 units, prices could still not increase.

If we want property prices to increase in line with the 2% to 3% annual productivity growth rate, then transaction volumes would need to increase significantly before annual price increases move beyond 2% to 3% a year.

There should be less fear of that now. If the measures are recalibrated wisely, the spike in transaction volume should not trigger a rapid asset price inflation. The reason is that there is enough headroom for transactions to increase by 50% without triggering sharp price increases unlike in the past.

In 2016, the new-home sales market improved significantly, increasing 7.1% y-o-y. Yet, at 7,972 units, it is still a far cry from the least upper limit of X + 10,000 (X because we do not yet know how much above 10,000 units that prices would start to increase). So, even if new-home sales were to rise 25.4% y-o-y to 10,000 units in 2017, it is unlikely to lead to price increases that are above the productivity growth rate of 2% to 3% (see Chart1).

The interim solution is a zero property price increase objective. This can be achieved even if new-home sales exceed 10,000 units a year. Achieving an increase in transaction volume would merely require some adjustments to the current slate of cooling measures.

Relationship between price changes and sales volume changes

It is common to expect that whenever sales volume increases, prices will react similarly. In simple terms, the ideal picture of how real estate prices and sales volumes behave are those data points falling within the blue shaded quadrants in Chart 2.

The message from Chart 2 is that both volume and prices are positively correlated in that, when volume increases, prices increase and vice versa. Thus, ideally, for any year, the relationship between the y-o-y change in sales transactions and y-o-y change in prices should be one that falls within the blue shaded quadrants in Chart 2.

For Singapore, for the period of 2005 to 2016, the two metrics of the private residential market were in the majority of observations of behaviour within that positive relation, but there were five instances or years in which the market strayed from expectation: 2009, 2011, 2013, 2015 and 2016 (see Chart 3).

For 2009 and 2013, the data points strayed because of the shocks from to the global financial crisis and the implementation of the TDSR respectively. That leaves 2011, 2015 and 2016, which did not face shocks, but displayed anomalies. In 2011, the government introduced two punitive measures: a hike in the seller’s stamp duty in January and the additional buyer’s stamp duty in December.

The red arrow points to the quadrant where these data points were in the quadrant where prices fell under the conditions of rising volumes in 2015 and 2016. The last two years saw a slowdown in the economy as plummeting oil prices took a toll on the offshore and marine sector, and the unemployment rate climbed.

A possible reason for the negative correlation could be the intensity of the property cooling measures, especially in 2013. This could put public and private policy decision makers in an uncomfortable position should immediate action for redress in the property market be taken.

--thisisapagebreak

Ideal vacancy rate

When we plot the movement of prices with vacancy rates for the period of 2005 to 2016 and overlay an annual price growth of 2% over it (the 2% is our long-term productivity growth rate), either strangely or coincidentally, the three intersection points of all three lines were at a vacancy level of 5.6% to 5.7%. Let us take 5.6%, as an example. For 4Q2016, the vacancy level for all local private residential properties was 8.1%, which is far above the 5.6% lifted off the graph (see Chart 4).

With vacancy levels significantly above the ideal level and expected to continue climbing this year, the concern is on the level of unproductivity in the real estate asset class. Supply from future land sales programmes should ideally be tempered to cure this excess.

Today, the elevated supply, coupled with slower rental demand arising from continuing global economic headwinds, should be able to alleviate fears that any tweaks to the cooling measures would bring about a V-shaped price recovery.

Although the stock of unsold units in the pipeline has been falling, this should not be used as a rationale for keeping the measures in its current intensity because total stock of units in the pipeline is still over 48,000 units. Therefore, even if new supply is maintained at current levels, the amount of slack created by the high levels of uncompleted stock may be enough to resist any upside price pressures (see Chart 5).

--thisisapagebreak

Rents — more sensitive to supply

Much of the talk about increasing economic value-add would come to naught if one merely focused on using supply to contain prices because prices tend to be less sensitive to supply. The supply mechanism is not effective in constraining prices but rents.

Any supply measure is therefore counterproductive when property yields fall too much. Chart 6 shows that the current net yield or return on invested capital (ROIC) for non-landed private residential property is 2.75% — well below the sector’s weighted average cost of capital of 5.74% (using the 3Q2016 average loan-to-value percentage of 52.6% and an unlevered beta of 0.38).

Conclusion

In many discussions about the cooling measures, “recalibrate” has often been confused with “removal”. And after witnessing 14 quarters of consecutive decline in the URA price index, the private residential market is starting to display a strange behaviour. This needs to be addressed.

First, the vacancy rate is at an unhealthy level, and by letting prices slide slowly, the overlooked point is that rents are coming off even more, and this destroys the economic value-add of real estate as an asset class. Future supply will have to take falling rental yields into consideration.

Second, the relationship between prices and transaction volumes are now out of sync. It should be an opportune time now to recalibrate the appropriate measures to bring market behaviour back to normal. As we are just outside the bounds of normal market behaviour, one need only to make minor adjustments to bring things back in line.

Alan Cheong is the head of research at Savills Singapore

This article appeared in The Edge Property Pullout, Issue 767 (Feb 20, 2017) of The Edge Singapore

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Subscribe to our newsletter

Search Articles